Solo Stove (NYSE: DTC) is down almost 50% YTD. Last week, it announced a leadership change and provided a voiceover on 2023 sales and adjusted EBITDA guidance. The stock fell sharply.

In this letter, I’m trying to understand if the company’s financials are underperforming or if there’s a disconnect with public markets (or both).

Let’s begin.

We’ll use the following structure for this breakdown:

- About the company

- Financial profile

- My observation

About The Company

Solo Stove is based in Grapevine, TX, and owns the following brands:

Company’s strategy is to buy and run omnichannel brands that leverages e-commerce, wholesale and retail presence to drive growth.

It was started in 2010 by two brothers, Spencer and Jeff. They started the company with $15,000. They eventually exited the business to private equity in 2019, and transitioned to advisory and board roles. A year after the initial PE transaction, they recapitalized the business again by selling to another PE group (2020). Eventually going public in 2021. It went from a Kickstarter campaign to a $2 billion valuation when it went public in 2021.

If you’re a DTC founder and operator, Spencer did a podcast in 2022, where he shares his story and lessons learned along the way: link here. Worth a listen.

In essence, Solo Stove is a house of brands. You can call them an aggregator if you like. I’ve previously written about why aggregators are late-cycle assets. Let’s dive into their financials to see why the company’s stock is struggling.

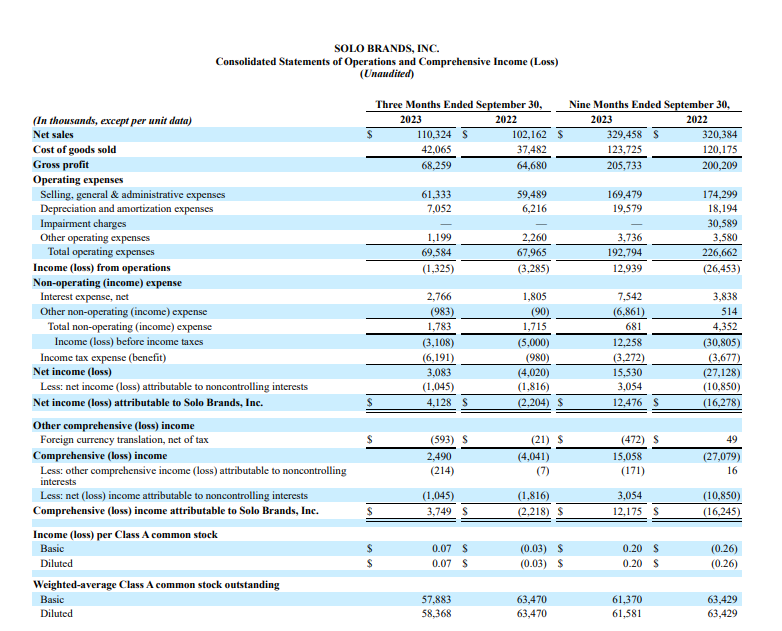

Financial Profile

I like to start with the balance sheet first. The last quarterly financials were released on 9/30/2023. Q4 ‘23 financials will come out in a few weeks.

One thing that stands out here is Goodwill and intangible assets. It’s a significant part of the total assets. For reference, Goodwill is typically added to B/S when one company acquires another through M&A. Intangibles are included when a brand has a strong reputation, copyrights, or other non-physical assets like patents, etc.

- Current ratio: 2.94 (good)

- Quick ratio: 1.13 (okay, needs to be above 1.0)

- Debt-to-Equity: 0.34 (good, low ratio)

Let’s dig into the income statement.

- Gross margin: 62%

- OPEX as a % of net revenue: 63%

- NOI%: -1.2%

- Interest expense as a % of net revenue: 2.5%

It looks like Solo Stove has non-controlling interests in some smaller DTC brands, which probably aren’t profitable. These are likely strategic investments allowing Solo Stove to purchase them when they’re the right size.

DTC is 70% of the business and 30% is wholesale.

I’m curious to see ad spend and marketing expenses breakdown to help gauge their contribution margin. This is what really matters for a company like Solo Stove since most of the business is DTC and they likely spend significant ad $ on customer acquisition. They’ve bucketed it all under “Selling, general & admin” on their P&L which would include salaries, wages, fixed and variable marketing expenses, rent, software, etc.

Cash Flow Statement

Notable items that stood out:

- Heavier focus on growth both organic and inorganic:

- Capex continues to be a focus; verticalization of the business will improve margins. They spent $6.9M on Capex.

- Cash spent on acquisitions (net of cash that was acquired from those acquisitions): $34.6M

- AP account is very low compared to the size of the company. Good work here by management. I’ve seen $15M companies with the same AP values as Solo Stove.

2023 Acquisition Activity:

- TerraraFlame: on May 1, 2023, Solo Stove acq TerrarFlame for $13.2M. They paid $5.5M cash at closing. The remaining $7.7M is for earn-out and post-closing payment obligations.

- Icy Breeze: On July 1, 2023, Solo Stove acq Icy Breeze for $52.1M. They paid $30M cash, net of $7.4M in cash acquired. Remaining $14.9M were based on contingencies in an earn-out capacity.

My Observations:

This looks like a good company with a decent financial profile, but the stock is struggling. TTM P&L:

- Total Revenue: $526.7M

- Gross Profit: $323.7M

- GM%: approx 62%

- OPEX: $283.9M

- Operating Income: $39.7M

- NOM%: 7.5%

The company’s current market cap (as of the time of this writing) is $278M. Which feels undervalued. Trading at approx 7X multiple. P&L profile is pretty standard to what I see in high-performing DTC brands. GM% can always be improved… I suspect some of the Capex will pay off long-term in margin improvements. Given the liquidity, solvency and overall health of the balance sheet, there aren’t any red flags that stand out. For PE, companies doing $40M+ in EBITDA are the holy grail. They can trade for 12-20X depending on operational complexity, competitive ecosystem, bolt-on acquisition potential, and financial health, amongst other variables.

The business should have strong opportunities to acquire more brands, verticalizing ops to improve margins and using learnings from one brand to another to influence more efficiency.

Enterprise values across the entire DTC ecosystem have compressed which creates a large pool of outdoor-focused brands for them to tuck in. Cost of capital going up likely prevents them from aggressively acquiring multiple brands in a year, but that’s not a bad thing.

FY 2023 guidance provided by the company:

- Revenue is now expected to be between $490 million and $500 million. This compares to our previous guidance of $520 million to $540 million.

- Adjusted EBITDA margin (1) is now expected to be in the range of 14% to 15%. This compares to our previous guidance of 17% to 18%.

Anyone who has worked with consumer product brands over the last decade is familiar with narrative adjustments. All things considered, not a real reason for the company to see a large dip in its stock price. Since going public, NYSE: DTC is down -83.33%.

This looks like a productive asset that’s struggling to perform in public markets. Maybe a large PE firm can purchase this at a discount, bring it back private, and when equity markets re-adjust, take it back out or exchange hands with another PE firm.

*Note: not investment advice. Nothing in this letter suggests the stock is being recommended for purchase. I’m not directly affiliated with the company in any capacity. No formal valuation methods were used. This was an afternoon scroll of financial statements with some notes on what I saw.