Many holding companies are being formed to roll-up DTC microbrands. It’s sort of like a micro-PE model. Let’s call it that for the sake of this discussion.

Large PE shops normally like to do deals at $500M+ value. Mid-market PE shops like to do deals between $100M-500M. Smaller PE shops like to do deals between $25M-100M.

If you’re unfamiliar, PE uses equity capital + co investments from LPs + debt to buy majority or minority shares in private companies.

Historically, anything below $25M hasn’t made sense for PE. You have Limited Partners (LPs) that are seeking a certain return and acquiring smaller companies versus larger companies requires the same amount of work. In fact, smaller deals often require more work because those companies have not been institutionalized. Their books are muddy, processes aren’t dialed in, etc.

Enter micro PE model. Doing deals in the long tail (below $25M). Rolling it up in a holding company model to maximize shareholder value. Sum of all is better than individual companies.

It’s never been easier to start a business. It’s never been harder to grow one.

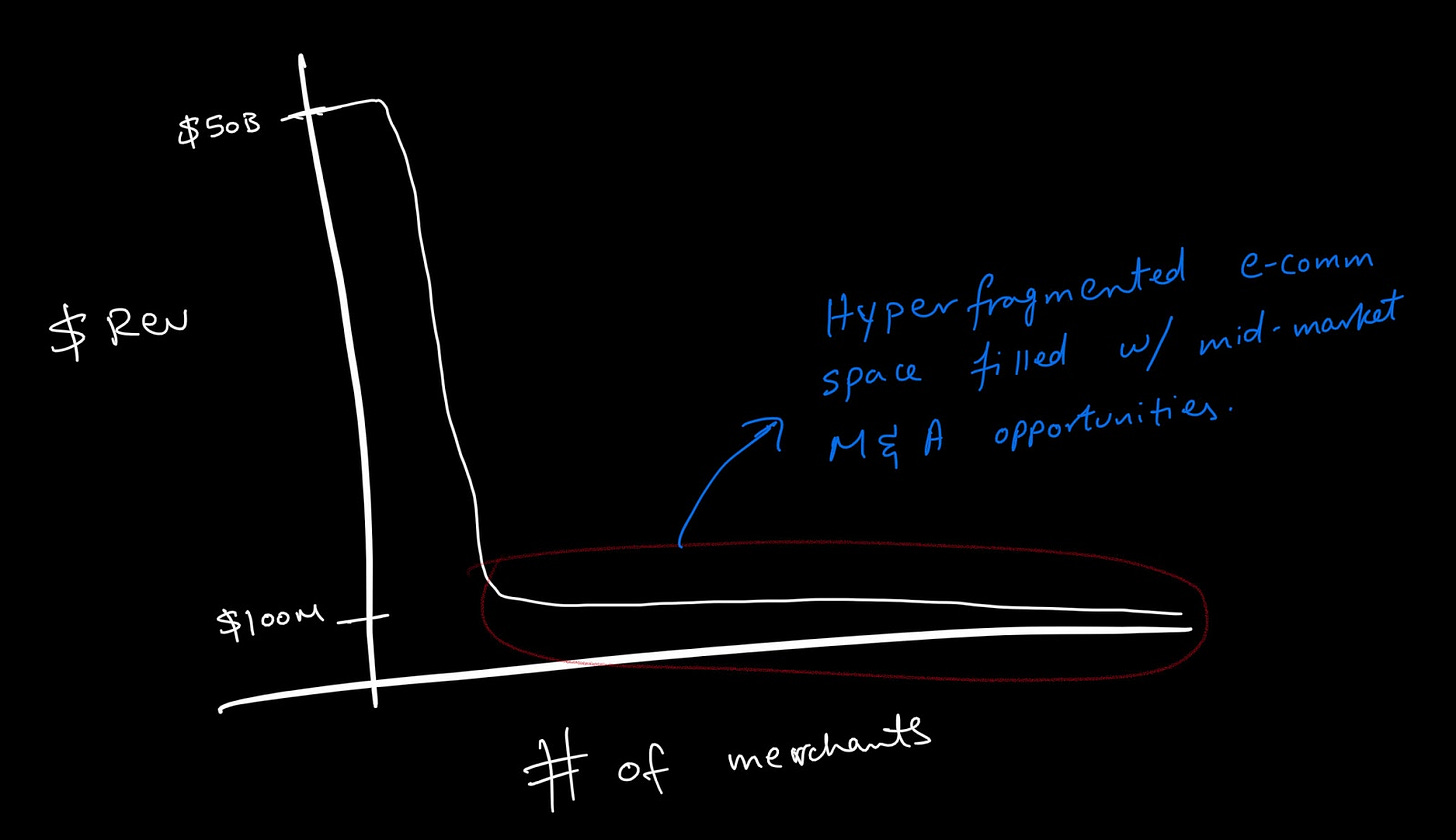

I discussed in 4 stages of growth for DTC brands that it’s challenging to grow beyond $25M in top line revenue. Brands often get stuck in stage 3 of growth.

M&A happens for a few reasons for DTC companies:

- Finding synergies & capabilities/distribution networks

- Adding revenue / EBITDA to the holding co structure

- Creating greater enterprise value

There’s a lot of liquidity in the market at this moment. Raising capital isn’t particularly difficult. I would argue that there’s a lot more capital than there are opportunities to put capital to good use. With interest rates being near zero and asset price inflation in full swing, investors are seeking illiquidity premiums and alpha in unique ways. Market conditions will likely change and evolve once rates go up (currently projected for 2023). Risk management will become key then and firms will have to adapt accordingly.

The tricky part is that most groups being formed that I’ve spoken to haven’t fully thought through integration challenges. Doing M&A isn’t particularly hard especially if you have access to deal flow. It’s the integration of suppliers, vendors, marketing teams, etc that’s hard.

If you’re a micro PE or holding co for micro-DTC, there are ways you can tackle this. This is based on my experience and what I would do if I owned the holding co:

- Have one accounting and finance function across all brands. Hire a great CFO.

- Have a dedicated demand forecasting team / program.

- If you operate within the same category but want to own multiple brands in that sector, then have one dedicated product and supplier relations team.

- Have a dedicated Retention and CRM team. Leverage those audiences across each brand in a PII-safe capacity where it makes sense.

- Build a back office for brand, creative and marketing. Leverage outsourced vendors and partners accordingly. You can get great value and competitive rates with partners when you bundle brands in a multi-brand capacity.

- Hire a GM for each brand that leads the brand and is a key member. If the brand is doing $10M+ in sales, convert that GM into a CEO and slowly build a team underneath him/her. Dedicated resources should only be given to brands doing more than a certain revenue threshold. $10M+ is arbitrary in this case. I picked this number because it’s officially a “stage 3 growth brand” that now requires more resources.

The challenge almost all large CPG companies face is that their family of brands don’t talk to each other. They live in their own silos. This is somewhat justified because of the supply chain complexities, shopper marketing activations, ERPs, etc. There are cross-functional efforts and resources for them to share notes and leverage opportunities where it makes sense; especially in omnichannel distribution networks.

It doesn’t really make sense to have dedicate brand functions when you’re a smaller company. Cross-functional teams can achieve greater outputs versus individual teams if people, process and tools are dialed in. Sharing resources also enables better margins and more scale.

Ultimately, holding co model can be effective if executed properly. General partners (GPs) that are leading M&A initiatives must have strong M&A experience and understand the value creation in e-commerce. DTC experience alone will not suffice. Best GPs will have strong PE and business operating experience.

Next 3-5 years will be interesting to see how this strategy comes to life.

This insightful discussion sheds light on the evolving landscape of private equity and the emergence of micro PE models. 💼💡 The strategy of aggregating DTC microbrands into holding companies below the traditional PE threshold is indeed a game-changer, offering solutions to the challenges of scaling for smaller businesses. 🚀 The focus on synergy, distribution enhancement, and revenue addition highlights the potential for maximizing shareholder value in a rapidly changing market. 💰 Exciting times ahead for both investors and DTC entrepreneurs! 🌟 #PrivateEquity #DTC #MicroPE #BusinessGrowth 📈