We’re living in a time where investors across every asset class are worried about the same thing: monetary policy and its impact on markets. From REIT fund managers to VCs investing in tech to PE folks investing in mid-market companies; all the way to retail investors.

There are two types of market environments: volatile and non-volatile. Market participants typically observe VIX as a measure for market volatility. VIX is a ticker symbol of volatility index, which measures the stock market’s expectation of volatility based on S&P 500 index options.

Broadly speaking, the world is long-assets and short-volatility.

Let’s zoom out and look at reasons why we’re observing market fragility:

- Fed suggested the word “transitory inflation” needs to retire; causing concern

- Fed’s tapering of QE starting March

- Fed raising interest rates to control inflation

- Russia-Ukraine conflict

- Supply chain constraints

There’s likely an exhaustive list of things we can add ranging from Evergrande’s debt obligation (largest real estate company in China), USA vs. China trade dynamics, China vs Taiwan, Canadian truckers protest… most people are less concerned about geo-political events since inflation typically overcomes all those issues.

Financial fragility is typically markets being vulnerable to a financial crisis. Given the low unemployment rates, strong demand and expected growth ahead are all positive signs of us coming out of the pandemic. Yet inflationary pressures prevent capital markets from feeling relaxed.

So, if inflation is the main problem, how do we solve for it?

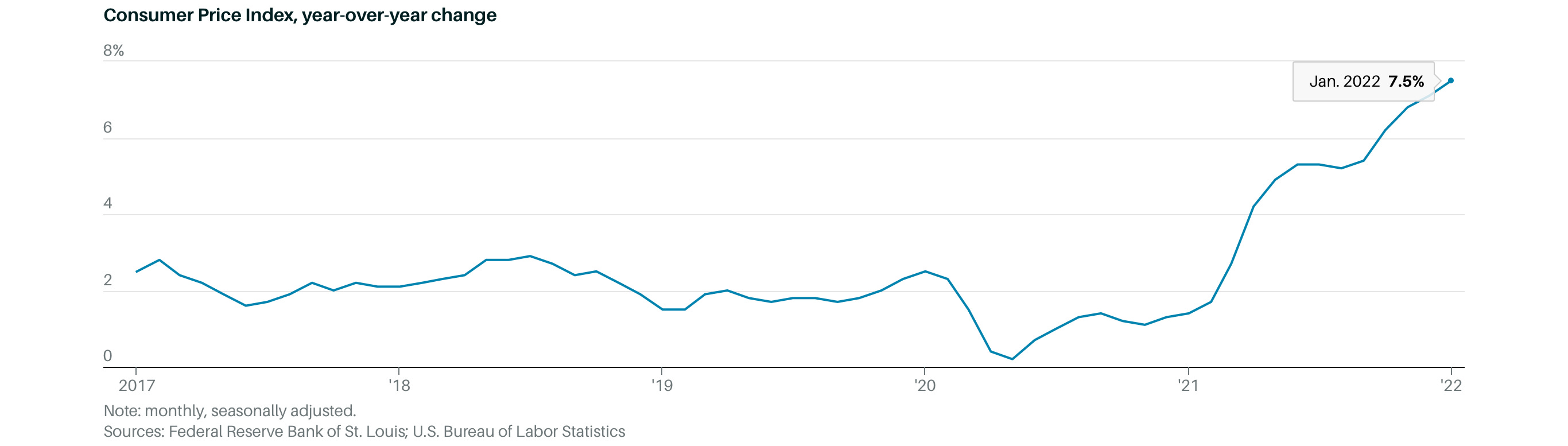

Not all inflation is bad. Historically, the US trends at ~2% inflation annually. This level of inflation feels healthy and encourages modest growth. It’s when CPI starts exceeding well beyond that baseline is when we start to worry. Our inflation rate has been steadily increasing in 2021; with latest CPI showing 7.5%.

The Fed has historically fought inflation by raising interest rates. The Fed is expected to raise rates 5 times minimum this year. I’d imagine these rate hikes will be modest; probably 250 bps each time.

History in motion: it’s not uncommon for the Fed to behave this way. In early 1980s, Paul Volcker was raising rates every Saturday for a brief moment to control inflation.

We’ll likely still see higher price premiums on certain items like cars, homes and others. And that’s because the market takes time to adjust to new monetary policy. There will also be other factors that play into those prices (e.g. supply chain constraints, China tariffs, supply-demand of certain items, etc).

Raising rates is the best tool the Fed has to combat inflation. There are other strategies the government can help the Fed with. This may include starting/managing a conflict with another nation (government spending drives GDP growth). A bit orthogonal, but causing a market correction with events-driven strategy isn’t out of reach. By depressing asset prices, they can influence consumption behavior.

How are investors navigating uncertainty and managing volatility?

- Dollar cost average; they’re still buying.

- Diversifying across all asset classes

- Underwrite the businesses they invest in; due diligence is key

- Using debt properly to hedge against inflation (e.g. real estate)

- Divorcing speculative assets

If you sell $50K in equities today, you now have a $50K problem. Where are you going to put that capital to use?

Cash is powerful but you want to be asset rich. The world is long assets, not long cash. Treat cash as your medium of exchange to buy high quality assets.

Every investor is feeling a pinch right now. Maybe the best thing to do is be patient and let things settle down before buying in again?

Everything we’re wrestling with right now is temporary. Zoom out 10-20 years into the future; will a few weeks of volatility change your investing thesis? Probably not.